First-Time Home Buyer Guide

A complete, jargon-free guide designed for New Hampshire buyers. Scroll through at your own pace, or jump to the section that matters most to you.

First-Time Home Buyer Guide

Hi, I'm Bryce

Your Guide Through This

I'm Bryce Broadhurst, a REALTOR® in New Hampshire who specializes in working with first-time home buyers. But more than that, I'm an educator. My job isn't to rush you into a purchase — it's to make sure you understand every step so well that you feel confident making the biggest financial decision of your life.

Most first-time buyers feel overwhelmed because nobody's ever explained the process in plain English. That's exactly what this guide is for. No jargon, no fine print tricks, no pressure.

Full Transparency

No hidden fees, no surprises

People First

Your timeline, your comfort, your pace

Educator, Not Salesperson

Understanding before action

Myth v. Reality

The 5 Biggest Myths Holding You Back

Let's bust the misconceptions that keep first-time buyers on the sidelines.

Myth #1

"You need 20% down to buy a home"

Reality

This is the #1 myth stopping buyers. In reality, FHA loans require just 3.5% down, and conventional loans can go as low as 3%. NH Housing has programs offering down payment assistance too. On a $300,000 home, that's $9,000–$10,500 instead of $60,000.

💡 Pro tip: Ask a lender about NH Housing's Home Flex Plus program.

Myth #2

"You need perfect credit to get approved"

Reality

FHA loans accept scores as low as 580 with 3.5% down. Even conventional loans typically require just 620+. Many lenders offer free credit consultations and can help you improve your score in 3–6 months.

💡 Pro tip: Don't check your credit through third-party apps — talk to a lender directly for an accurate picture.

Myth #3

"Renting is always cheaper than buying"

Reality

In many NH markets, a mortgage payment on a starter home is comparable to rent. Plus, every payment builds equity in YOUR asset. Rent increases are unpredictable. A fixed-rate mortgage stays the same for 30 years.

💡 Pro tip: Use the rent vs. buy calculator on this site to see real numbers.

Myth #4

"You should wait for rates to drop"

Reality

While rates fluctuate, home prices in NH have historically trended up. Waiting for a 1% rate drop could mean paying $30,000+ more for the same house. You can always refinance your rate later — you can't refinance your purchase price.

💡 Pro tip: 'Marry the house, date the rate' — refinance when it makes sense.

Myth #5

"Open houses are enough research"

Reality

Open houses show you the surface. Real research means understanding the neighborhood, school districts, flood zones, tax rates, future development plans, and comparable sales. That's what an agent does for you.

💡 Pro tip: I provide a detailed market analysis for every property my clients consider.

Down Payment

3–20%

$9,000–$60,000

On a $300K home. Most first-timers put down 3–5%.

Closing Costs

2–5%

$6,000–$15,000

Title insurance, attorney fees, recording fees, lender fees.

Earnest money

$1,000–$5,000

Typically 1–3%

Shows you're serious. Goes toward your purchase.

Home Inspection

$400–$700

One-time cost

Crucial. Never skip this. Catches problems before you own them.

Homeowners Insurance

$100–$250/mo

Required by lender

Protects your investment. Shop around for rates.

Property Taxes

Varies by town

NH avg: ~$23 per $1K

NH has no income or sales tax, but property taxes vary drastically.

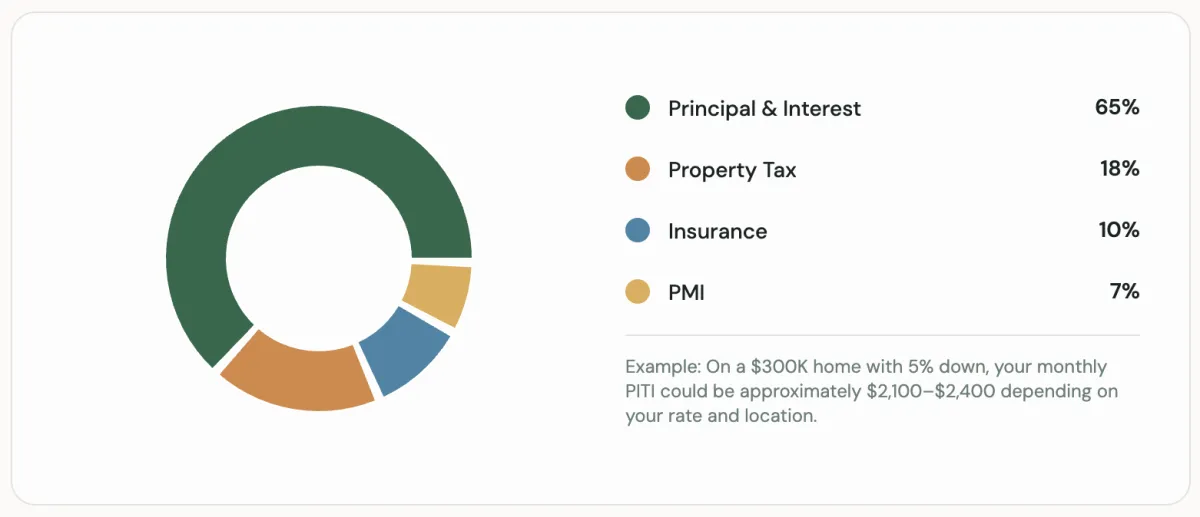

What's Inside Your Monthly Payment?

get started

The Ideal Home Is Waiting for You

lorem ipsum Quam est faucibus porttitor luctus sem phasellus. Pretium neque aliquet .

The Journey

Your Step-by-Step Roadmap

From finances to front door. Here's every milestone, explained simply.

Prepare Your Finances - 2-6 Months Before

Check credit, save for costs, get documents ready. Think of this as your foundation.

Get Pre-Approved - Week 1

A lender reviews your finances and tells you what you can borrow. This is your shopping budget.

Start Your Home Search - Weeks 2-8

I set up targeted searches based on your needs, not just price. Quality over quantity.

Tour Homes and Showings - Ongoing

I'll point out what you can't see — roof age, water damage signs, neighborhood factors.

Make an Offer - When ready

I'll help craft a competitive offer based on market data, not emotion.

Negotiate - 1-3 Days

Counteroffers, concessions, terms. I handle this so you don't have to stress.

Home Inspection - Within 10 days

A professional examines the home top to bottom. We negotiate repairs if needed.

Appraisal - 2-3 weeks

The bank confirms the home is worth what you're paying. This protects you.

Final Walk Through - 1-2 days before closing

One last look to make sure everything is as agreed. Repairs done, home clean.

Closing Day - 30-45 days from offer

Sign the papers, get the keys. Your chosen title companies agent and I will be right there with you.

Move In! - You choose

Welcome home. I'll be here if you need anything — even recommendations for pizza.

Your dream team

Building the Right Team Around You

You don't do this alone. Here's who's in your corner and what each does for you.

Your Realtor (Me)

What I do

Guides the entire process, negotiates on your behalf, coordinates with everyone.

When

Day 1 through closing and beyond

💡 Think of me as your project manager. I keep everything on track.

Mortgage Lender

What they do

Reviews your finances, gets you pre-approved, and funds your loan.

When

Step 1 — before you even look at homes

💡 A good lender educates you on options, not just sells you a rate.

Title Company

What they do

Reviews contracts, handles the closing, ensures your legal protection.

When

After your offer is accepted through closing

💡 I have trusted partners that I can recommend, but you're free to shop

Home Inspector

What they do

Examines the home's condition — structure, systems, safety issues.

When

After your offer is accepted (within 10 days typically)

💡 Never skip the inspection. A few hundred dollars can save you thousands.

Insurance Agent

What they do

Sets up your homeowners insurance policy, which your lender requires.

When

Before closing

💡 Get quotes from multiple agents. Bundling with auto insurance often saves money.

Contractor (if needed)

What they do

Handles repairs or renovations identified during inspection or after purchase.

When

After inspection or after closing

💡 I have a trusted network of local contractors I can refer you to.

learn from others

5 Mistakes First-Time Buyers Make

These are avoidable. And now that you know about them, you'll avoid them.

Shopping before getting pre-approved

You might fall in love with a home you can't afford. Or worse, lose it to a buyer who IS pre-approved.

➡ Talk to a lender first. Know your number before you start looking.

Draining your entire savings for the down payment

You still need money for closing costs, moving, repairs, and an emergency fund. Being house-rich and cash-poor is stressful.

➡ Keep at least 3 months of expenses in reserve after closing.

Ignoring monthly budget reality

A lender will tell you the maximum you can borrow — but that doesn't mean you should borrow the max.

➡ Calculate what you're comfortable paying each month, including all housing costs.

Waiving the home inspection

In hot markets, some buyers skip inspections to 'win' the offer. This can lead to $10,000+ in unexpected repairs.

➡ Always get an inspection. If a seller won't allow one, that's a red flag.

Getting emotionally attached too early

When you're in love with a house, you overpay, overlook problems, and make emotional decisions.

➡ Stay analytical until you're under contract. There will always be another home.

Don't worry, I can help!

Understanding The Market

Market Terms in Plain English

The real estate market isn't as complicated as it sounds. Here's what actually matters.

Interest Rates

= "The cost of borrowing money"

Think of it like rent on the money you borrow. A lower rate means a lower monthly payment. Even 0.5% makes a big difference over 30 years. Current rates fluctuate, but historically we're still in a reasonable range.

Inventory / Supply

= "How many homes are for sale"

Low inventory means fewer choices and more competition. NH has had tight inventory for years, which is why preparation and speed matter. Being pre-approved gives you an edge.

Multiple Offers

= "When several buyers want the same home"

In competitive markets, this happens often. I'll help you craft an offer that stands out — it's not always about the highest price. Terms, timing, and flexibility matter too.

seller concessions

= "When the seller pays some of your costs"

In some situations, sellers will contribute to your closing costs. This is more common when a home sits longer on market. I'll help you know when and how to ask.

Days on market

= "How long a home has been listed"

Fewer days = hotter property. More days = potential for negotiation. Homes sitting 30+ days often have motivated sellers. This is valuable information for your offer strategy.

Seasonal Trends

= "When it's best to buy in NH"

Spring and summer are busiest (more competition). Fall and winter often have less competition but fewer listings. There's no perfect time — the best time is when YOU're ready.

How I work

A Different Kind of Agent

Here's what working with me actually looks like

Communication That Works for You - Text, call, email, video — whatever you prefer. I respond quickly and I explain things clearly. No question is too basic.

Technology That Saves You Time - Online document signing, virtual tours, automated search alerts, and market dashboards. Modern tools for modern buyers.

Strategic Negotiation - I use market data, not gut feelings. Every offer is backed by comparables, trends, and a strategy to get you the best deal possible.

Education-First Philosophy - I'll never push you to buy. Instead, I'll teach you how to evaluate homes, read contracts, and make confident decisions.

Complete Transparency - You'll see every number, understand every fee, and know exactly what's happening at every stage. No black boxes.

Your Questions Answered

Frequently Asked Questions

No question is too basic. Here are the ones I hear most often.

How much money do I actually need to buy a home?

For a $300,000 home in NH, you might need as little as $12,000–$20,000 total (3.5% down + closing costs). There are also down payment assistance programs that can reduce this further. I'll connect you with a lender who can run your specific numbers.

What credit score do I need?

FHA loans accept 580+, conventional loans typically require 620+. But don't get hung up on a number — talk to a lender. Many buyers are surprised to learn they qualify sooner than they think.

How long does the whole process take?

From pre-approval to closing, typically 45–90 days once you find a home. The pre-approval itself takes 1–3 days. Finding the right home can take a few weeks to a few months depending on the market.

Do I have to pay you out of pocket?

All real estate commissions are negotiable. Most sellers offer concessions for buyer's agent representation. This is something that I will help you negotiate into your offer. You get professional representation without having to bring the full amount to the closing table. I'll explain exactly how this works during our first meeting.

What if I find problems during the inspection?

That's the whole point of the inspection — to find problems before you own them. We can negotiate repairs, credits, or even walk away if the issues are serious. The inspection protects you.

Should I sell my current place before buying?

It depends on your situation. Some buyers can carry two mortgages briefly. Others need to sell first. A lender can help you understand your options, and I can help coordinate the timing.

What's the difference between pre-qualified and pre-approved?

Pre-qualification is a quick estimate. Pre-approval is a thorough review of your finances with documentation. Sellers take pre-approval much more seriously. Always aim for pre-approval.

Can I buy a home if I have student loans?

Absolutely. Lenders look at your debt-to-income ratio, not just whether you have debt. Many buyers with student loans qualify for mortgages. A lender can show you exactly how your loans affect your buying power.

What are closing costs and who pays for them?

Closing costs are fees for the loan, title, attorney, and other services — typically 2–5% of the purchase price. Buyers usually pay these, but sometimes sellers will contribute. We can negotiate this.

How competitive is the NH market right now?

NH has been a competitive market with limited inventory. But that doesn't mean it's impossible — it means preparation matters more. Pre-approved buyers with a strong agent have a real advantage.

Helping home buyers and sellers in New Hampshire navigate the journey with clarity and confidence.

Email: [email protected]

Mobile: (603) 490-0904

Office: (603) 637-4818

605 Pine Street Manchester, NH 03104

Galactic Realty Group LLC

quick links

Copyright 2026. Bryce Broadhurst. All rights reserved.